In its new strategic Mid-Year Outlook report on European equities, Morgan Stanley puts Greece in a particularly favorable transition point, among emerging and developed markets, as the Athens Stock Exchange prepares to gradually move into the new category of major international indices.

The key message from the house is that the Greek market is not just facing a technical upgrade event, but a period in which it may attract increasing interest from developed market investors, at a time when emerging market investors do not appear to be completely abandoning Greek exposure.

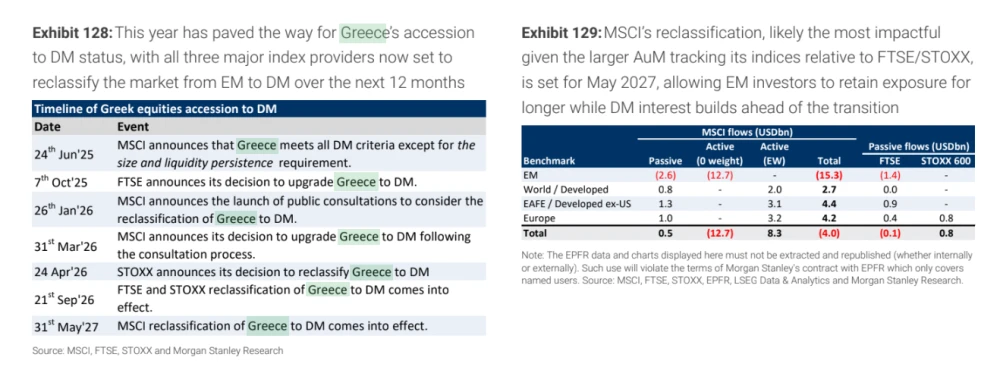

Morgan Stanley believes the MSCI upgrade will be the most significant in terms of long-term and passive funds, as the funds under management tracking MSCI indices are around twice as large as those tracking the FTSE.For MSCI, the house estimates mild net passive inflows of $0.5bn, or around two days of trading coverage. The more interesting point, however, is that Morgan Stanley does not see the exit from emerging markets as a net negative event. While Greece is already overweight for several emerging market portfolios, the firm’s discussions with investors indicate continued interest in maintaining exposure, either outside the index or through custom mandates.

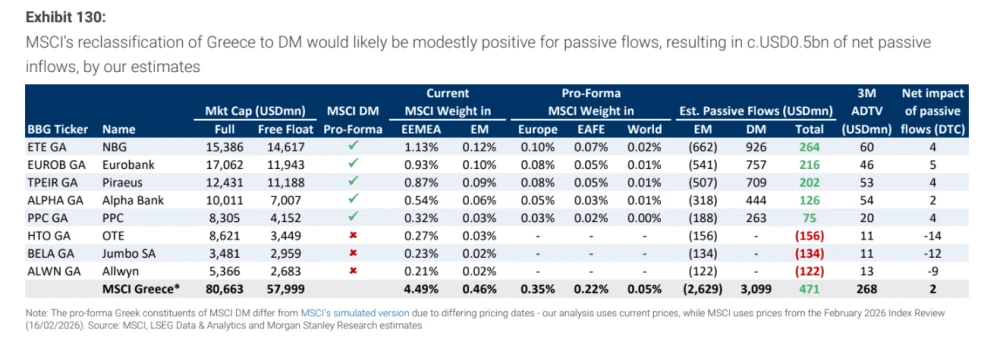

The data shows that passive inflows are not evenly distributed, but are concentrated almost exclusively in stocks that pass through the developed market profile. National Bank has the largest net positive result, with estimated net passive inflows of $264m, followed by Eurobank with $216m, Piraeus Bank with $202m, Alpha Bank with $126m and PPC with $75m. In contrast, OTE, Jumbo and Allwyn are not included in Morgan Stanley’s developed markets profile and have estimated outflows of $156m, $134m and $122m, respectively. Thus, the overall net picture for MSCI Greece remains positive, with $471m of net passive inflows, but the real benefit is mainly for the four systemic banks and PPC.

How the stock picture is linked to the outperformance of the economy

This picture is linked to the macroeconomic outperformance of the country. Morgan Stanley highlights that private consumption and investment are the key drivers of Greek resilience. The Recovery Fund has supported investment activity and, although the programme expires in December 2026, the firm expects investment levels to remain strong into 2027, given the time lag of around two years between the receipt and utilisation of funds.

On the country risk front, Morgan Stanley notes that the Greek 10-year bond yield is now moving closer to the European periphery, in line with France and even lower than Italy. At the same time, the country has undertaken significant deleveraging, while Greek banks have cleaned up their balance sheets, with the NPL ratio down to low single digits at 3.6%.

The key point for valuations is that despite the improvement in bonds and fundamentals, the Greek market’s cost of equity remains high relative to Europeople. Morgan Stanley puts the Greek cost of equity margin over Europe at around 440 basis points, compared with a long-term average of around 240 basis points. A return to the historical average would imply a 27% upside margin, all other factors held constant, according to the house.

Morgan Stanley’s preference for the Greek market runs mainly through banks. This is no coincidence, as banks make up 77.2% of MSCI Greece, compared with just 13.7% in MSCI Europe. For the house, Greece remains a market where the history of upgrading, macroeconomic resilience, improving country risk and bank profitability are combining in a rare transition phase.

Source:Newmoney.gr